The Town's plan for Route 132 bond payments will need adjustment

It means an automatic 4.9% budget increase in 2022.

When the 2021 municipal budget was drafted, it was relying on an estimated debt service schedule for the anticipated "up to" $4 million bond to repair Route 132. The project was awarded to Northwoods Excavating, who bid $3,198,000. In addition, the $4 million figure included estimated costs associated with repairs on the Strafford-side of Route 132: $184,664 estimated for guardrails and signage, and $254,109 estimated for the topcoat, striping, and road shoulder finish work.

The estimated schedule had the Town paying $15,988 in interest in 2021, and no principal. The 2021 budget, however, sought to raise $118,000. The idea was simple: there would be an estimated 2021 "surplus" of $102,012, which could be applied to the bond payment in 2022, estimated to be $314,235 (interest plus principal). This "surplus" would mean that the town would only have to increase tax revenue by an estimated $94,223 in 2022 to meet its obligations ($118,000 increase from 2021 plus $102,012 surplus from 2021 equals $220,012, or $94,223 shy of the $314,235 estimated payment for 2022). In 2023, there would be another approximately $100,000 increase since there would be no more previous year "surplus" to offset the need for new tax revenue.

The intention was that the budget increase would be staggered over three years (approximately a 3.6% increase per year), instead of hitting the budget all in one year (approximately a 10.8% increase over 2020, all else the same).

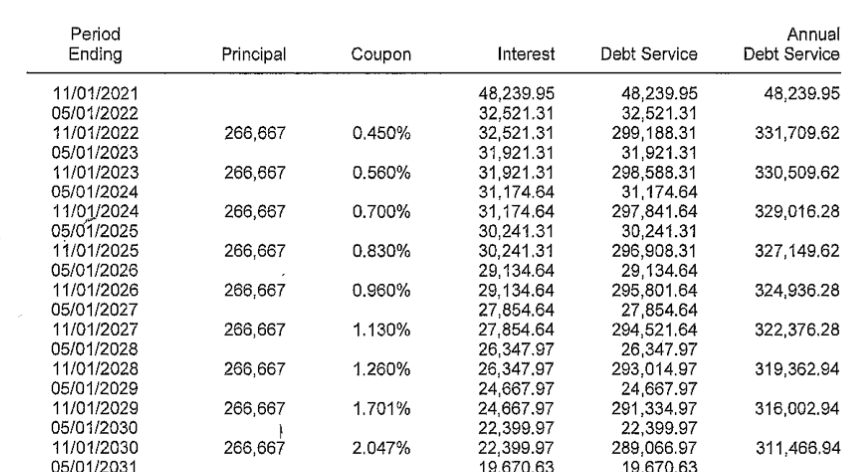

The estimated debt schedule was produced in September of 2020 for budgeting purposes, with the expectation that there would be some variance depending on the fluctuation in interest rates between then and closing. The estimated closing for the bond was for late July of 2021. However, instead, the Town closed on the loan in early March of 2021, roughly five months earlier than it had estimated. Instead of the estimated interest payment of $15,988 that was budgeted for, the additional five months of interest accrual (plus any changes to interest rates) resulted in an actual 2021 interest payment of $48,240, a difference of $32,252. For context, this difference represents about 1.1% of the total municipal tax revenue for 2021.

This means the "surplus" from 2021's $118,000 is down to $69,760. And the actual payment for 2022 is up as well, from the estimated $314,235 to an actual $331,710. The Town will need to raise $143,950 in new taxes in the 2022 municipal budget to make this commitment, $49,727 more than it was expecting during budget season last year. In sum, the 2022 increase would represent a 4.9% increase over 2021 municipal tax revenue, up from an estimated increase of only 3.2%. This means, all else the same, that tax revenue will have to increase an automatic 4.9% just for Route 132, before any other increases, such as those resulting from increased healthcare costs or union contract negoitations.

How did this happen? The Vermont Bond Bank has two loan pools per year, winter and summer. The estimated debt service schedule was relying on the assumption that the Town would enter the summer loan pool, thus closing on the loan later in the year and accruing less interest. Instead, the Town entered the winter loan pool. When the Town closed, the $4 million was immediately transferred, meaning that interest began accruing on the full $4 million immediately as well. It is not a line of credit where the Town draws only what it needs over time; that would make paying bond investors a fixed return unreliable.

While costs associated with Route 132 did begin in the spring (a first payment of $68,545 was made on April 30th to Stantec Engineering), the first payment to Northwoods Excavating was not until June. If the Town had stayed with the summer loan pool, it would have had to pay such costs upfront until it closed, a total of $436,633 according to invoices, which would have saved taxpayers $32,252 in accrued loan interest. However, it also would have meant drawing on the Town's cash on hand, which it needs for other obligations, such as payroll. Was there enough cash on hand, between the public works fund balance and Paving Fund (which recently received an unbudgeted $100,000 contribution from 2020 budget surplus) to make it work? Could some upfront costs have been delayed until after a summer loan closing?

Asking these questions now is too little too late, of course. All this unfolded during transitions among three Town Managers, including one part-time Interim Town Manager. Perhaps a consistent manager would've yielded better planning, but, unfortunately, this is what we have.